|

1) My friend and veteran investor Doug Kass of Seabreeze Partners published this missive yesterday, making a compelling case that any recession will be mild and brief:

Why I See a Mild and Brief Recession

* Consumer 'Cassandras' are multiplying

* But it is important to note the strong position of the U.S. consumer

* Consumers' ratio of liabilities to net wealth is at the lowest level in 50 years!

Over the last five weeks I have argued that there are substantive and underappreciated "buffers" that will likely serve as a ballast to the U.S. economy and are likely to lead to only a mild and brief recession, which would have less impact on U.S. corporate profits than the consensus increasingly expects.

The following factors support my case:

* The absence, in large part, of the sort of leveraged positions and segments of the economy that have characterized previous deep economic down cycles.

* Unlike previous economic downturns, especially the global financial crisis, our banking system is far less levered and has sizeable cushions of liquidity and capital.

* There is over $2 trillion of excess consumer savings.

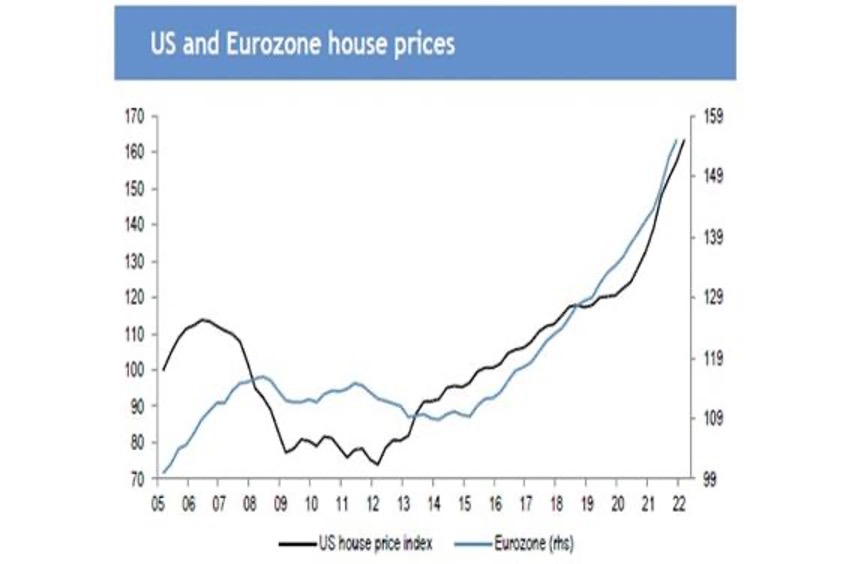

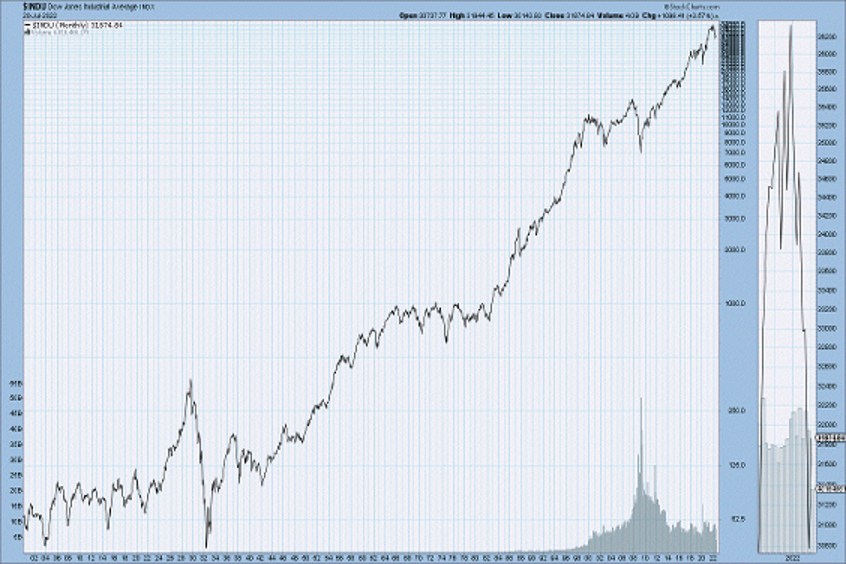

* There is a cushion of sizeable unrealized/embedded gains in the nation's housing stock and large unrealized gains in the U.S. stock market:

* The U.S. has a very strong industrial/corporate base that has generally improved their balance sheets by rolling over into inexpensive debt over the last five years, and that have maintained high profit margins.

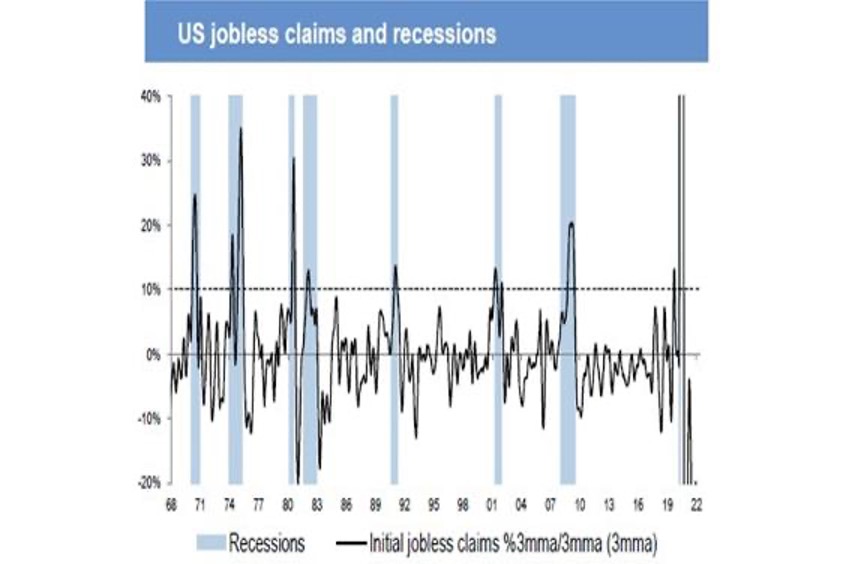

* We have a robust and tight labor market, with solid wage increases in the last several years. Importantly, in the last 60 years the U.S. has never had a recession without a preceding spike in initial jobless claims:

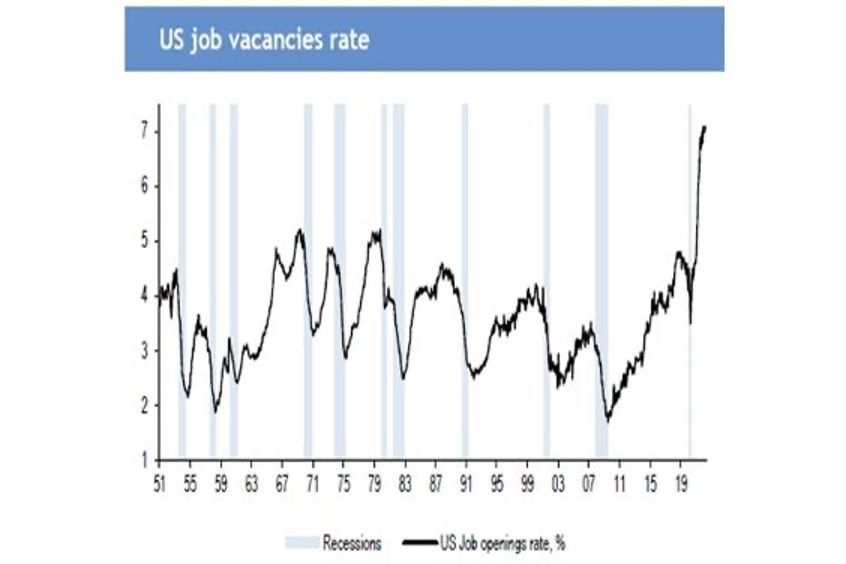

The job vacancy rate is at an all-time high:

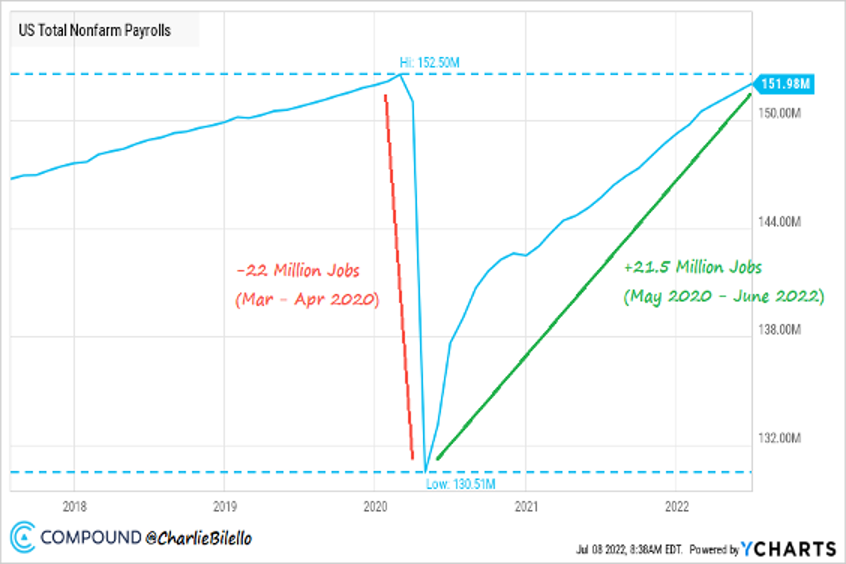

And the U.S. has almost fully recovered the jobs lost in the early months of the pandemic:

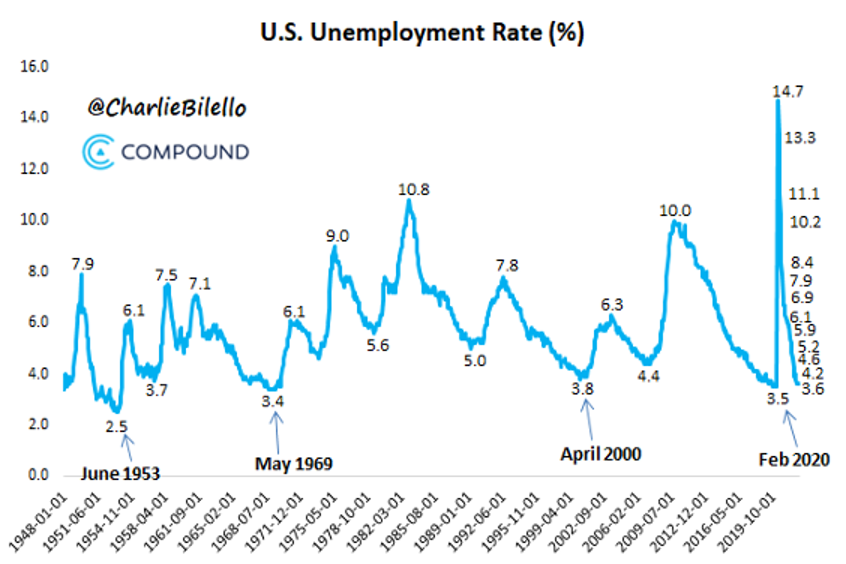

* The U.S. unemployment rate is 3.6%, the lowest level since the start of the pandemic and only 0.1% above the 50-year low reached just before the pandemic in February 2020:

* Some important components of inflation are moderating. The prices of most commodities have fallen considerably over the last two and a half weeks. Copper is down 33% from its all-time high in March and at its lowest level since 2020:

Corn, wheat, and soybeans are all down over 25% from their highs and below the levels they were at before Russia invaded Ukraine:

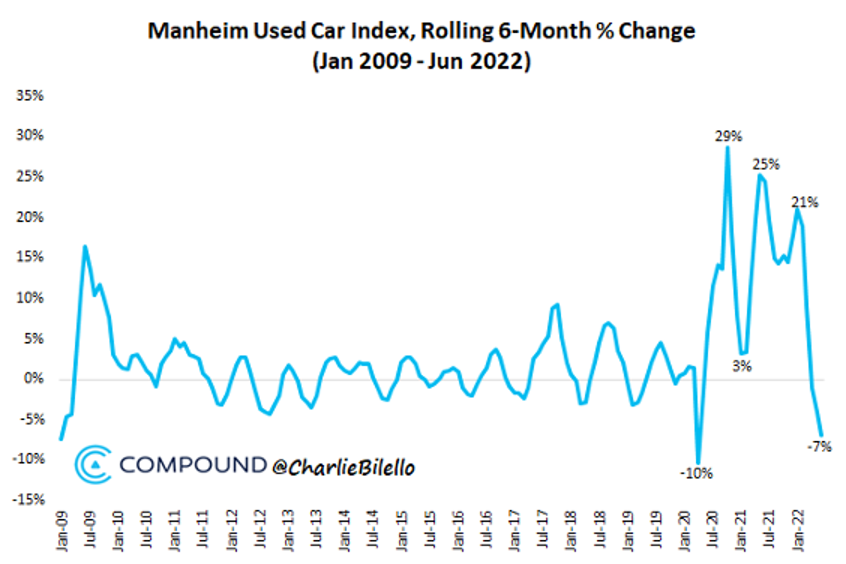

After spiking last year, used car prices are down 7% over the last six months:

Finally, the price of energy products has also fallen precipitously:

* Interest rates may have peaked. The yield on the 10-year U.S. note is about 40 basis points below its recent high.

* Several measures of supply chain health have begun to show signs of improvement. Deep sea freight costs (the black line in the below chart), which have been a good proxy for supply chain disruptions, dropped in June. And the New York Fed economists' Global Supply Chain Index (the red line) has fallen to the lowest level since March 2021:

Figure 1: PPI for Deep Sea Freight (black, left) and the GSCI (red, right)

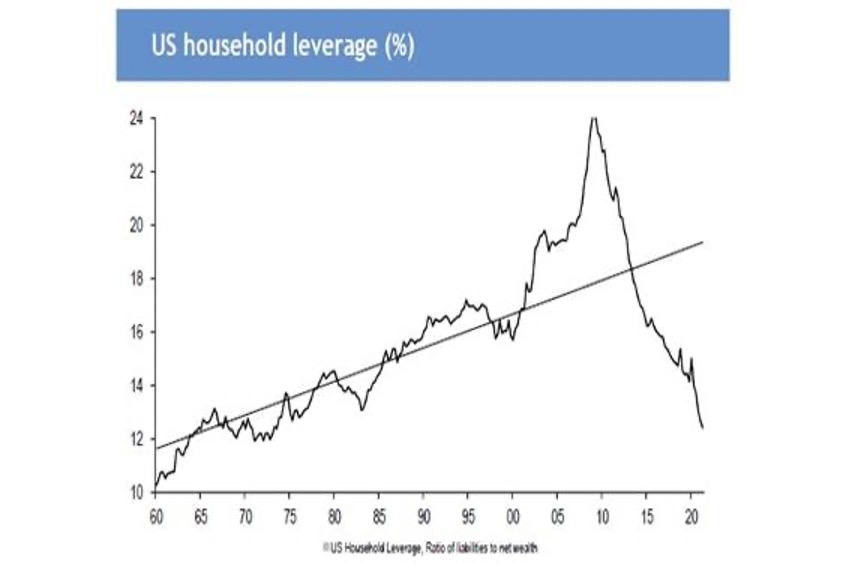

* To the many market participants who are focused on prospective consumer weakness due to the fall in mortgage activity and the marked decline in stocks, I offer the following chart, which demonstrates that consumers' balance sheets remain strong and underleveraged:

Indeed, as demonstrated above, the consumers' ratio of liabilities to net wealth is at the lowest level in 50 years!

Thank you Doug!

2) I gotta tip my hat to Mandeep Manku of hedge fund Coltrane Asset Management for having the courage of his convictions.

He was early in betting against growth stocks in 2020 and suffered mightily as they ripped upward, saddling him with a horrific 56% loss that year and shrinking his assets under management from over $1 billion to $200 million at the start of this year.

But rather than shutting down, he stuck to his guns and has been rewarded, as this Wall Street Journal article notes: One Hedge Fund Is Up 223% This Year Thanks to a Big Bet Against Tech Stocks. Excerpt:

While growth-focused hedge funds were recording steep losses and companies were slashing their valuations, Coltrane reaped profits.

Declines in the stock prices of pandemic darlings like Netflix (NFLX) and Peloton (PTON) contributed, as did shorts on Meta Platforms (META), videogame platform Roblox (RBLX) and electric-truck maker Rivian (RIVN), investors said.

A bet against used-car website Carvana (CVNA), whose stock price has plunged about 90% this year, contributed 9 percentage points of the gains, said a person familiar with the fund.

Mr. Manku and his team kept the trade on for two years, adding to bets as stock prices fell and cycling companies in and out of the trade. Coltrane placed bearish options bets that supercharged its returns, all while avoiding pressure to shut down.

"He's a conviction manager," said Stuart Roden, an early Coltrane investor and ex-chairman of European hedge-fund firm Lansdowne Partners. "He didn't get out at the wrong time. That's extremely difficult."

Mr. Roden said he wasn't as worried about the trade, whose analytical foundations he believed were sound, as he was about whether Mr. Manku would be able to see it through. "In our industry, lots of people who ended up right weren't able to be there when they were right because they were closed out or clients took their money away."

There are a few lessons here...

First, Manku's experience underscores how hard it can be – and how long it can take – to tell the difference between being wrong and being early.

Second, shorting is a really tough business, and the vast majority of investors would be better off if they never do it.

And lastly, the vast majority of investors should also never take the big risks that led to Coltrane's wildly gyrating performance. It reminds me of something investing legend Charlie Munger once said:

If you run through a dynamite factory with an open torch and happen to make it to the other side without blowing yourself to kingdom come, that doesn't mean it was a good idea!

3) On Monday, we're closing one of the best offers we've ever made since launching Empire Financial Research in 2019...

It's a way to get six free months of my Empire Investment Report, six free months of my friend Louis Navellier's Breakthrough Stocks, a free year of his Portfolio Grader, a model portfolio of 10 little-known stocks to buy today, and more.

This presentation will go offline on Monday, so if you haven't watched it, I'd urge you to take a look soon. You can watch it (or read a transcript) by clicking here.

4) I'm in Eugene, Oregon for the last three days of the World Track and Field Championships with my cousin and his family.

Here we are with the statue of legendary Oregon runner Steve Prefontaine, who finished fourth in the 5,000-meters in the 1972 Olympics and set many American records in distances, from the mile to the 10,000-meters. Tragically, while training for the 1976 Olympics in 1975 at age 24, he was driving drunk, flipped his car, and died.

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.

Will This New Technology Put Trains and Airlines Out of Business?

An incredible new technology could soon get me from my home in Manhattan to Washington, D.C. for as little as $25! This is likely to make a lot of people rich. Click here for my analysis, where I include the stock and ticker symbol of my No. 1 way to play it. |

|